In recent years we have received from religious institutes and affiliated ministries a number of requests for assistance with unraveling the notices they have received from the IRS with regard to their requirement to file Form 990. A number of organizations have been notified that their tax-exempt status has been revoked, and they find themselves listed on the IRS' list of revoked organizations. This can be devastating for the organization itself as it affects not only the organization's ability to receive tax-exempt donations but also their donors' ability to claim a charitable deduction for their donations. Once their name appears on the list, donors are deemed to have notice of the revocation and can be penalized for claiming a charitable deduction for their donations.

Most of the organizations that contact us in these situations were not required to file a Form 990. This means that they should not have been penalized for non-filing. However, the IRS may not know the reason for the non-filing exemption with respect to your religious institute. If your organization has received notices asking for your Form 990 in the three years leading up to the revocation, your response (or lack thereof) can be important to how the IRS will respond to the attempt to clarify the situation.

Generally, when we are contacted, we help the Treasurer of other business office personnel construct a letter explaining to the IRS that a Form 990 was not required to be filed based on the exemption for the "exclusively religious activities of any religious order" in IRC section 6033(a)(3)(A)(iii). Sometimes the exemption that applies is for an "integrated auxiliary" under IRC section 6033(a)(3)(A)(i). The test for an integrated auxiliary must be satisfied in this latter case and may require additional explanation.

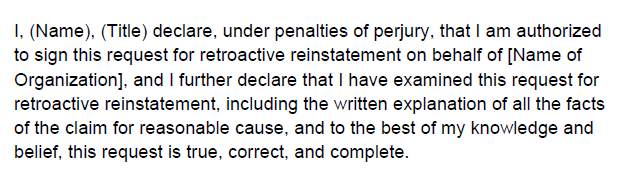

The reason for bringing up this Revenue Procedure is that it contains some specific language that would be wise to adapt and include in your letters when corresponding with the IRS on matters related to Form 990. This is true whether you are responding to a notice asking why you did not file a Form 990 for a given year or if you receive the dreaded notice that your tax-exempt status has been revoked. The pertinent part is in Section 8.06 (pages 7-8) of the Revenue Procedure. Below is the paragraph that the IRS recommends should precede the signature of a request for retroactive reinstatement.

Although you technically will not be asking for reinstatement if you were not required to file a Form 990 in the first place, it is important to indicate that you are aware of the requirements of the regulations that govern the (non-)filing of Form 990.

This is an extremely critical area of law, and the success or failure in resolving these IRS notices will affect, among other things, your institute or ministry's ability to not pay taxes on any and all income and your donors' ability to claim a deduction for donations made to your charitable organization(s).

No comments:

Post a Comment